If you own property in Pakistan, understanding the distinction between FBR property valuation and provincial DC rates is crucial for calculating your tax obligations accurately. Property taxes in Pakistan operate through a complex dual system—one managed by the Federal Board of Revenue (FBR) for federal taxes and another administered by provincial governments for stamp duty and registration fees. For both filers and non-filers, property tax calculations determine significant financial burdens during purchase, ownership, and sale.

The Federal Board of Revenue recently updated valuations for 56 cities across Pakistan starting November 1, 2024, introducing changes that directly impact property investment decisions and real estate market dynamics. Meanwhile, provinces like Punjab have shifted toward capital-value-based property taxation systems, further complicating tax planning for property buyers and investors.

This comprehensive guide explains how FBR valuations differ from DC rates, which system applies when, and how to calculate your actual property tax liability across Pakistan's major cities. Whether you're a first-time buyer in Lahore, an investor considering Karachi properties, or assessing property holdings in Islamabad, this article breaks down every component of Pakistan's property tax framework.

What Is FBR Property Valuation in Pakistan?

FBR property valuation represents the minimum value the Federal Board of Revenue assigns to immovable properties for federal tax purposes. Under Section 68(4) of the Income Tax Ordinance 2001, the FBR establishes these valuations to prevent tax evasion through underreporting property prices.

Key characteristics of FBR valuation:

- Applies to immovable property including residential plots, houses, apartments, and commercial properties

- Updated periodically through SRO (Statutory Rules and Orders) notifications

- Mandatory for calculating federal advance taxes, capital gains taxes, and withholding taxes

- Cannot be declared at values lower than FBR rates without facing penalties

- Applies uniformly across all properties in specified categories within defined areas

When you purchase property in Pakistan, the transaction value must equal or exceed the FBR valuation for that property location. The FBR determines these rates based on property types, geographic locations, and market analysis conducted by the Revenue Division.

For example, if FBR sets a residential plot valuation at 1 million rupees per marla in a Lahore development, you cannot register your purchase below this rate. The federal government uses FBR valuations as reference benchmarks to ensure adequate tax collection and prevent artificial undervaluation of properties.

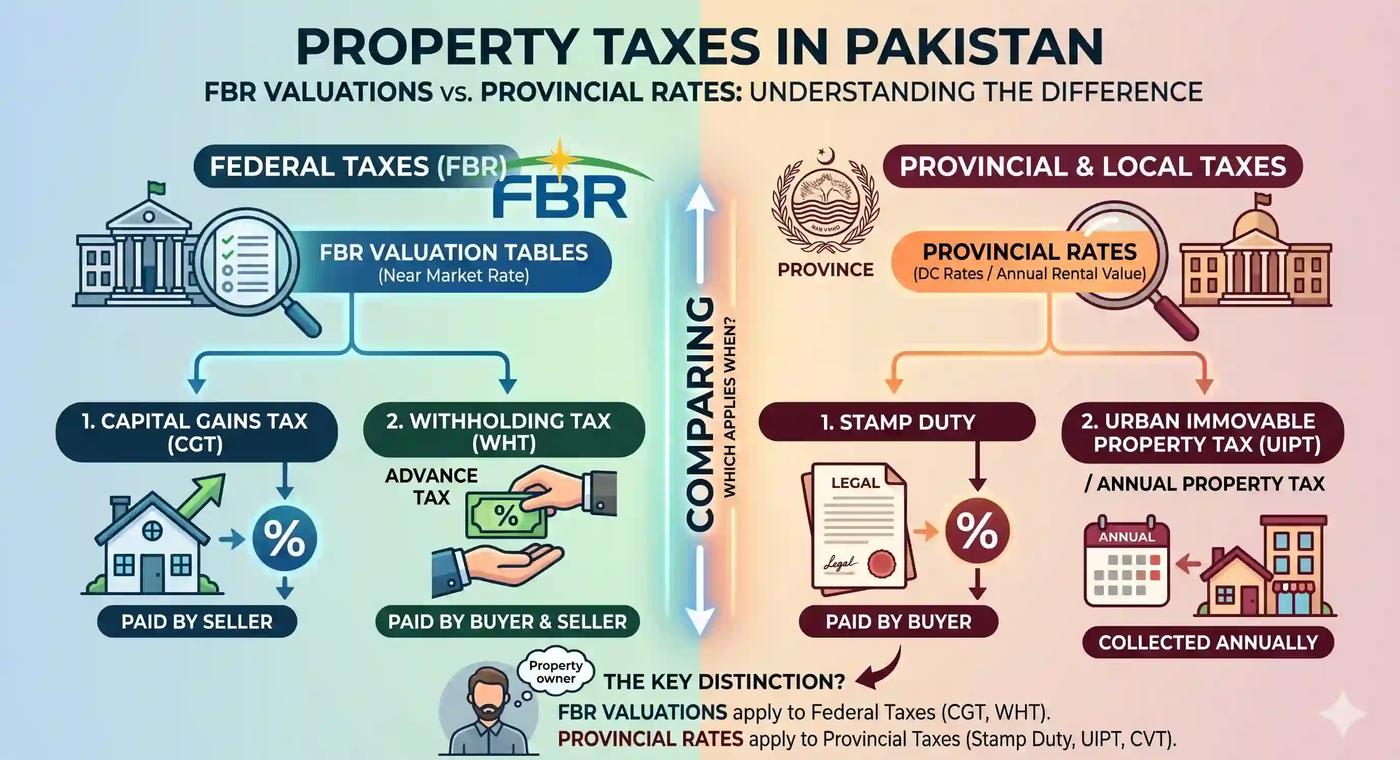

What Is the Difference Between FBR Rates and DC Rates Pakistan?

Understanding the distinction between FBR rates and DC rates is essential because they serve different purposes in Pakistan's property tax system, and both must be considered during transactions.

FBR Rates (Federal Valuations)

- Purpose: Calculate federal advance taxes (Section 236K for buyers, Section 236C for sellers), capital gains tax, withholding tax, and income tax

- Authority: Federal Board of Revenue

- Coverage: 56 major cities across Pakistan

- Application: Mandatory floor value—properties cannot be transacted below FBR rates

- Frequency: Updated periodically (most recently November 2024)

- Applies to: All property categories—residential, commercial, agricultural, and industrial

DC Rates (Provincial Valuations)

- Purpose: Calculate provincial stamp duty, registration fees, and transfer taxes

- Authority: Deputy Commissioner (DC) offices in respective districts

- Coverage: All districts in each province

- Application: Used for stamp duty calculation; often lower than FBR rates

- Frequency: Updated by provincial governments independently

- Applies to: Property registration and provincial tax collection

The Critical Difference: FBR valuation is higher and mandatory for federal taxes, while DC rates are typically lower and used for provincial stamp duty. During a property transaction, you pay taxes based on both systems—federal taxes using FBR rates and provincial taxes using DC rates.

Real-World Example: If you purchase a residential property in DHA Lahore:

- FBR valuation: 50 million rupees

- DC rate: 35 million rupees

- Federal advance tax (Section 236K, 2% for filers): 1 million rupees

- Provincial stamp duty (varies by Punjab rates): calculated on a different percentage

How Property Tax Is Calculated in Pakistan for Different Taxpayer Categories

Property tax calculations in Pakistan depend heavily on your filer status, property type, and the transaction nature. Non-filers face significantly higher tax burdens—typically 2x to 3x greater than filers.

For Filers (Active Taxpayer List Members)

Filers enrolled in the Active Taxpayer List (ATL) benefit from reduced property tax rates:

- Advance Tax (Section 236K for buyers): 0.5% to 2% of property value (depending on property type and location)

- Capital Gains Tax: 5% to 15% for properties held under 2 years; exemption for holdings exceeding certain periods

- Withholding Tax: Reduced rates on property transactions

- Registration and Stamp Duty: Provincial rates apply, typically 4-6% of transaction value

For Non-Filers

Non-filers pay substantially higher taxes:

- Advance Tax (Section 236K): 5% to 7% of property value

- Capital Gains Tax: Charged at 35-40% for short-term holdings

- Withholding Tax: Higher percentage deductions from seller's proceeds

- Registration and Stamp Duty: Standard provincial rates plus additional penalties

For First-Time Buyers

First-time property buyers in Punjab benefit from concessional rates if they are registered as filers, with reduced stamp duty and registration fees under provincial incentive schemes.

Understanding Section 236K and Section 236C: Advance Taxes on Property Transactions

These two sections of the Income Tax Ordinance 2001 govern advance tax collection on property transactions and represent critical compliance points.

Section 236K: Advance Tax on Property Buyer

Section 236K requires the property buyer to pay advance tax at the time of registration:

- Tax Rate: 0.5% to 2% for filers; 5% to 7% for non-filers

- Payer: Buyer of the property

- Assessment: Based on FBR valuation or transaction value, whichever is higher

- Payment Timing: Due at the time of property registration

- Documentation: Paid through property registration authorities or online platforms

Example: A filer purchasing a property valued at FBR rate of 10 million rupees pays 1% advance tax = 100,000 rupees immediately.

Section 236C: Advance Tax on Property Seller

Section 236C applies to property sellers and is deducted from their sale proceeds:

- Tax Rate: 0.5% to 2% for filers; 5% to 7% for non-filers

- Payer: Deducted from seller's proceeds during transaction

- Assessment: Calculated on FBR valuation or transaction value

- Deduction: Withheld by the buyer or his agent and deposited with FBR

- Adjustment: Can be claimed as credit against final tax liability

Property Tax Rates in Pakistan for Non-Filers vs. Filers: A Comprehensive Breakdown

The financial impact of non-filer status on property ownership is substantial. Here's how rates differ across major transactions:

| Property Tax Rates in Pakistan for Non-Filers vs. Filers | |||

|---|---|---|---|

| Tax Component | Filer | Non-Filer | Difference |

| Advance Tax (Purchase) | 0.5-2% | 5-7% | 5-7x Higher |

| Capital Gains Tax | 5-15% | 35-40% | 3x Higher |

| Withholding Tax | Reduced | Standard | 2-3x Higher |

| Annual Rental Value | 5% | 12.5% | 2.5x Higher |

| Total Estimated Tax Burden on 10M Property | 800K-1.5M | 5M-7M | 5-8x Higher |

This disparity explains why many property investors prioritize becoming filers before major real estate transactions. The savings frequently exceed 4-6 million rupees on significant property purchases.

FBR Property Valuation for 56 Cities: November 2024 Update and Impact

The Federal Board of Revenue's November 2024 revision updated property valuations across 56 major Pakistani cities, including all provincial capitals and secondary cities. This update represents one of the most significant FBR valuation revisions in recent years.

Cities Covered in FBR 56-City Valuation System

Punjab:

- Lahore (including DHA, Bahria Town, Capital Smart City, Blue World City)

- Rawalpindi (including Cantonment Board areas)

- Faisalabad

- Multan

- Gujranwala

- Sialkot

- Bahawalpur

Sindh:

- Karachi (all zones: South, East, Central, West)

- Hyderabad

- Sukkur

Khyber Pakhtunkhwa:

- Peshawar

- Abbottabad

- Mardan

Balochistan:

- Quetta

Impact on Property Market

The November 2024 FBR revision increased valuations in high-demand areas by 15-30%, directly impacting:

- Advance tax obligations during purchase and sale

- Capital gains tax calculations

- Withholding tax deductions

- Property registration costs

- Investment feasibility assessments

Property investors must recalculate investment returns using updated FBR rates, as higher valuations increase the total tax burden on transactions.

Capital Gains Tax on Property in Pakistan: Holdings, Rates, and Exemptions

Capital gains tax on property became increasingly important after July 1, 2024, when new regulations took effect for properties acquired on or after this date.

Capital Gains Tax Rates and Holding Periods

For Properties Acquired After July 1, 2024:

- Holding Period 1 Year or Less: Charged as ordinary income at slab rates (15-35% for non-filers, 5-15% for filers)

- Holding Period 1-2 Years: 20% tax (filers); 35% (non-filers)

- Holding Period Over 2 Years: Exemption from capital gains tax for filers; significantly reduced rates for non-filers

- Agricultural Properties: Separate treatment under agricultural income provisions

For Properties Acquired Before July 1, 2024:

- Grandfathering provisions apply; owners locked in at lower tax rates

- Properties acquired before 2024 benefit from exemptions not available on newly purchased properties

- This creates incentive for documenting acquisition dates correctly

Strategic Implications

Property investors face timing considerations—holding periods affect final tax liability substantially. A property generating 2 million rupees profit experiences vastly different tax outcomes:

- Held under 1 year: ~700,000 rupees tax (non-filer at 35%)

- Held over 2 years: Zero tax for filer, significantly reduced for non-filer

Stamp Duty and Registration Fees on Property in Pakistan by Province

While FBR manages federal taxes, provincial governments collect stamp duty and registration fees through their respective Excise and Taxation departments.

Provincial Stamp Duty Rates (Typical Structure)

Punjab (As of 2025):

- Residential property: 4% stamp duty + 1% registration fee (filers); 6% + 2% (non-filers)

- Commercial property: 5% stamp duty + 1.5% registration fee

- Agricultural property: 3% stamp duty + 1% registration fee

- Lahore capital value-based system: Different calculation method

Sindh:

- Capital value tax (CVT) replaces traditional stamp duty

- Calculated on declared value; rates vary by area

- Commercial zones: Higher CVT rates than residential

Khyber Pakhtunkhwa:

- Standard stamp duty: 3-4% for residential

- Registration fee: 1%

- Property tax exemption applies for certain categories

- KPK property tax calculator available for quick estimation

Balochistan:

- Stamp duty: 4% for residential property

- Registration fee: 1%

- Balochistan property registration handled through district administration

Total Transaction Cost Example

Purchasing a 15-million-rupee residential property in Lahore (for a filer):

- FBR advance tax (Section 236K, 2%): 300,000

- Stamp duty (4% on DC rate): ~400,000

- Registration fee (1%): ~100,000

- Total Federal + Provincial Taxes: ~800,000 (5.3% of transaction value)

Adding this to purchase costs is essential for investment calculations.

DHA Property Tax, Bahria Town, and Other Housing Societies: Special Considerations

Gated communities and planned housing societies have unique property tax characteristics because they span across different valuation zones.

DHA Property Tax Across Cities

DHA Lahore:

- FBR valuation highest among Pakistani housing societies

- Ranges from 80-150 million per 5 marla depending on phase

- Stamp duty and registration typically 5-6% combined

- Capital gains tax considerations critical for short-term sales

DHA Rawalpindi:

- Lower FBR valuations than Lahore

- Cantonment Board taxation applies in some areas

- Property tax rates Rawalpindi include cantonment surcharge

DHA Karachi:

- Follows Sindh CVT system

- Different tax treatment than federal FBR system

- Capital value tax Karachi rates significantly lower than FBR equivalents

Bahria Town and Private Housing Societies

- Not subject to FBR valuations uniformly across all projects

- Each Bahria Town development (Bahria Town Lahore, Bahria Town Karachi, Bahria Town Rawalpindi) has separate FBR guidelines

- Community management fees separate from property taxes

- Capital gains treatment same as conventional properties

Blue World City and Capital Smart City

These mega projects in Islamabad follow FBR valuation rates for Islamabad but sometimes feature developer financing arrangements affecting tax calculations. Property tax Blue World City Islamabad and property tax Capital Smart City require individual assessment based on plot sizes and locations.

Property Tax in Cantonment Areas: Special Rules and Calculation Methods

Cantonment areas across Pakistan (Rawalpindi Cantonment, Lahore Cantonment, Karachi Cantonment) follow different taxation rules administered by Cantonment Boards rather than municipalities.

Cantonment Property Tax Calculation

- Annual Rental Value Approach: Property tax calculated at 15% of annual rental value

- Exemptions: Military personnel and certain service categories enjoy exemptions

- Cantonment Board Authority: Separate from FBR and provincial excise departments

- Additional Charges: Community services charges in addition to property tax

Example - Rawalpindi Cantonment: A residential property with estimated monthly rental value of 50,000 rupees:

- Annual rental value: 600,000

- Property tax: 15% = 90,000 annually

- Plus additional cantonment services levy

Provincial Property Tax Variations: Punjab, Sindh, KPK, and Balochistan

Each province administers property taxes distinctly, requiring province-specific knowledge for accurate compliance.

Punjab Property Tax System (2025)

Punjab recently transitioned to a capital-value-based property tax system starting January 2025:

- Calculation: Based on declared capital value rather than annual rental value

- Tax Rate: 0.2% to 0.4% annually on declared capital value

- Applicable: Lahore capital value based property tax 2025 and other major cities

- Impact: Shift from rental value assessments to market value assessments

Sindh Capital Value Tax (CVT)

Sindh implements Capital Value Tax as its primary property tax mechanism:

- Coverage: All properties in Karachi, Hyderabad, and other Sindh cities

- Rates: Progressive based on property value and category

- Assessment: Conducted by Excise and Taxation Department

- Rate: Capital value tax Karachi Sindh typically 2-4% depending on property classification

KPK Property Tax System

KPK maintains traditional property tax frameworks:

- Basis: Annual rental value or market value assessment

- Rates: 5-10% of annual rental value for residential properties

- Exemptions: KPK property tax exemption applies for certain categories including properties owned by widows, disabled persons, and students

- Calculator: KPK property tax calculator available online for preliminary estimates

Balochistan Property Tax

Balochistan property registration and taxation handled through district administrations:

- Method: Property assessment conducted by district revenue offices

- Rates: Vary by district and property type

- Registration: Compulsory before taxation liability attaches

How FBR Valuation Affects Property Prices and Market Dynamics

FBR property valuation adjustments create ripple effects throughout Pakistan's real estate sector:

Immediate Market Impacts

When FBR raises valuations significantly (as in the November 2024 revision):

- Buyer Hesitation: Potential buyers reassess investments due to increased tax burdens

- Price Negotiations: Sellers often adjust nominal prices lower to compensate for higher FBR-based taxes

- Market Volume Decline: Transaction volumes typically decrease until market adjusts to new valuations

- Investment Recalculation: Property investment returns decline due to tax burden increases

Long-Term Market Effects

- Affordability Crisis: Higher FBR valuations reduce affordable property availability

- Rental Market Shift: Some investors convert purchase-intent into rental holdings due to reduced purchase ROI

- Institutional Investment: Increased interest from institutional investors with broader financial capacity

- Tax Compliance Improvement: Higher FBR valuations reduce gap between declared and market values

The 2024 FBR revision impacted property prices in 56 cities, with high-value locations like DHA and Bahria Town experiencing particularly significant adjustments.

How to Calculate Property Tax in Pakistan: Step-by-Step Process

Step 1: Determine Filer Status

Verify whether you're registered as a filer with FBR's Active Taxpayer List (ATL). Non-filers face 5-7x higher tax rates.

Step 2: Identify Applicable FBR Valuation

Check current FBR valuation rates for your property's location using the FBR property valuation rates 2024 complete list. Visit the official FBR website or use a property tax calculator Pakistan 2026 for accurate determination.

Step 3: Calculate Advance Tax (Section 236K for Buyers)

- Filers: FBR valuation × 0.5% to 2% (varies by property type)

- Non-Filers: FBR valuation × 5% to 7%

Step 4: Determine Provincial Stamp Duty and Registration

- Filers: DC rate × applicable percentage (typically 4-5%)

- Non-Filers: Higher rates apply; check province-specific rates

Step 5: Assess Capital Gains Tax (If Applicable)

- Properties held under 2 years: Standard slab rates apply

- Properties held over 2 years: Tax exemption for filers

- Calculate gain = Sale Price - Original Purchase Price

- Apply appropriate capital gains tax rate

Step 6: Use Interactive Calculators for Accuracy

Rather than manual calculation prone to errors, use interactive property tax calculators offered by Tax Calculators (https://taxcalculators.tools/tools/pk/property-tax-calculator) which update automatically with new FBR rates and provincial variations.

Reducing Property Tax in Pakistan: Strategies for Buyers and Investors

Become a Filer Before Property Purchase

The single most impactful tax reduction strategy—transitioning from non-filer to filer status reduces tax burden by 500-700%.

Process:

- Register with FBR as individual taxpayer

- Obtain National Tax Number (NTN)

- File annual tax returns showing sufficient income

- Obtain Active Taxpayer List (ATL) status confirmation

- Document ATL status before property transaction

Time Property Transactions Strategically

Purchasing property toward end of tax year allows holding until next calendar year before sale, potentially triggering capital gains exemptions (if applicable).

Utilize First-Time Buyer Benefits

Punjab and other provinces offer stamp duty reductions for first-time buyers registered as filers. Ensure proper documentation of first-time status during registration.

Consider Joint Ownership

Structuring property ownership between spouses or other family members may trigger different tax treatment under certain provincial laws. Consult tax professionals for jurisdiction-specific guidance.

Structure as Inheritance Rather Than Purchase

Inherited property faces different tax treatment than purchased property in some situations. Gifted property in Pakistan FBR assessment differs from inherited property tax treatment.

Explore Tax-Planning Through Multiple Transactions

Some investors structure larger acquisitions as multiple smaller transactions to maintain holdings below certain thresholds triggering higher capital gains rates. (Requires professional guidance to avoid FBR challenges.)

FAQ: Commonly Asked Questions About Pakistan Property Tax

Q: What is the difference between FBR rates and DC rates in Pakistan?

A: FBR rates are federal valuations for calculating advance taxes, capital gains tax, and withholding taxes—typically higher and mandatory floor values. DC rates are provincial valuations used for stamp duty and registration fees—usually lower. Both apply during transactions, but for different purposes.

Q: How much property tax do non-filers pay compared to filers in Pakistan?

A: Non-filers pay 2-3 times higher property taxes than filers. On a 10-million-rupee property purchase, non-filers might pay 5-7 million rupees in total taxes versus 1.5-2 million for filers—a difference of 3.5-5.5 million rupees.

Q: Can FBR valuation be higher than DC rate?

A: Yes, FBR valuations are consistently higher than DC rates. This is intentional design—FBR valuations establish the minimum transaction floor for federal tax purposes, preventing undervaluation.

Q: What is section 236K advance tax on property?

A: Section 236K of the Income Tax Ordinance 2001 requires property buyers to pay advance tax at registration time. Filers pay 0.5-2% while non-filers pay 5-7% of FBR valuation.

Q: Is there property tax exemption for senior citizens or widows in Pakistan?

A: Yes, certain provinces offer exemptions. In KPK, widows and disabled persons benefit from property tax exemptions. Punjab offers reduced rates for specific categories. Check provincial government websites for current exemptions.

Q: Which 56 cities are covered under FBR property valuation?

A: The 56 cities include all provincial capitals (Lahore, Karachi, Islamabad, Peshawar, Quetta), major secondary cities (Rawalpindi, Faisalabad, Multan, Gujranwala, Sialkot, Hyderabad, Sukkur, Abbottabad, Mardan, Bahawalpur) and their associated planned communities like DHA branches, Bahria Town developments, and other major housing societies.

Q: How often does FBR revise property valuations?

A: FBR revises property valuations annually or as needed based on market conditions. The most recent comprehensive revision occurred November 1, 2024. Future revisions typically follow similar annual patterns.

Q: What is capital gains tax on property sold within one year in Pakistan?

A: Properties sold within one year of acquisition incur capital gains tax at ordinary income slab rates: up to 35% for non-filers and 5-15% for filers, depending on total income slabs.

Q: What happens if property is registered below FBR valuation in Pakistan?

A: Registrations below FBR valuations face rejection by registration authorities, or if accepted, trigger FBR investigations, penalties, and forced revaluation with additional tax demands plus interest charges.

External Resources and Official References

For authoritative information on Pakistan property taxation, consult these official sources:

- Federal Board of Revenue (FBR): https://www.fbr.gov.pk/ - Official FBR website with valuation notifications and tax regulations

- State Bank of Pakistan Real Estate Sector: Official guidelines on real estate taxation compliance

- Income Tax Ordinance 2001: Complete text available through National Assembly legislative website

- Provincial Revenue Divisions: Each province maintains property tax guidance through respective revenue departments

Real Estate Investment Tax Considerations: Strategic Planning for Modern Investors

Property investment in Pakistan requires sophisticated tax planning given complexity of FBR vs. provincial systems, filer vs. non-filer disparities, and capital gains treatment variations.

Investment Decision Framework

Pre-Purchase Tax Assessment:

- Calculate complete tax burden using current FBR rates and provincial rules

- Compare investment returns after-tax across potential projects

- Evaluate filer status benefits—often worth pursuing ATL registration before major transactions

- Model capital gains scenarios under different holding periods

Portfolio Structuring:

- Diversify across provinces to leverage varying tax treatments

- Consider rental income vs. capital appreciation tax implications separately

- Structure holdings across family members to optimize aggregate tax burden

- Time acquisitions and sales strategically within calendar/financial years

Post-Acquisition Planning:

- Track property improvements separately (impact cost basis for capital gains)

- Document holding periods meticulously (critical for exemptions after 2 years)

- Monitor FBR revisions affecting property valuations

- Reassess annual through online property tax status

Conclusion: Navigating Property Tax Complexity in Pakistan

Property taxation in Pakistan presents significant financial implications for all owners and investors. Understanding the distinction between FBR valuations and provincial DC rates, recognizing filer vs. non-filer disparities, and optimizing transaction timing can result in substantial savings—often exceeding millions of rupees on major properties.

The November 2024 FBR revision across 56 cities underscores the importance of staying current with regulatory changes. Whether you're purchasing in Lahore's DHA developments, investing in Karachi's growing commercial sectors, acquiring property in Islamabad's new smart cities, or exploring Rawalpindi's cantonment areas, professional tax assessment ensures compliant transactions minimizing your final tax burden.

Take action today: Use interactive calculators and professional consultation before finalizing property transactions. The difference between calculated property taxes and actual obligations often exceeds the cost of professional guidance.

Explore our Advanced Free Tax Calculators: Visit Tax Calculators' property tax calculator to instantly calculate your exact property tax obligations based on current FBR valuations, provincial rates, and your filer status. Our calculator updates automatically with new 2024-2025 rates, ensuring you always reference current regulations.

For advance tax calculations on property transactions, try our advance tax calculator to determine Section 236K and 236C obligations immediately.

Don't navigate Pakistan's complex property tax system alone. Professional assessment protects your investment and ensures compliance with federal and provincial requirements.

Important disclaimer

This article is for educational planning only. It does not provide professional tax, legal, accounting, payroll, customs, or financial advice. Tax rules can change and final results may depend on your personal facts. Always verify important tax decisions with official sources or a qualified professional.